The Income Tax Act, 1961, has officially been repealed. From April 1, 2026, a brand new law governs how India pays its taxes, and the changes are bigger than most people realise.

For HR professionals, payroll managers, and working Indians, this isn’t just a legal overhaul happening somewhere in the background. It directly affects how salaries are structured, how Tax deduction at source (TDS) is calculated, which city employees can claim 50% HRA, and how your organisation files its returns. Here’s a plain-language breakdown of what’s changed and what it means for you.

The Big Picture: A 65-Year-Old Law Gets Replaced

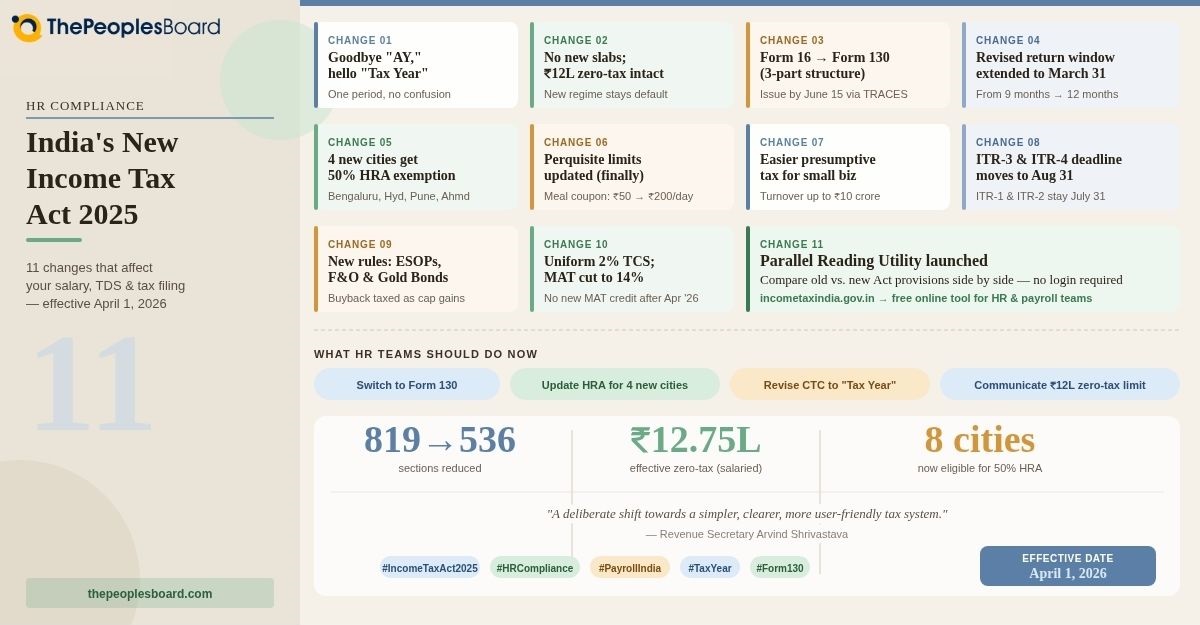

India’s Income Tax Act, 1961, survived over 4,000 amendments across six decades. By the time it was retired, it had grown into a document of 5.12 lakh words across 819 sections, which Finance Minister Nirmala Sitharaman described as a “maze.”

The Income Tax Act 2025, effective April 1, 2026, replaces it with the stated goals of lowering errors, disputes, and compliance costs. The new law has been compressed significantly:

- Sections: Reduced from 819 to 536

- Chapters: Reduced from 47 to 23

- Word count: Cut from 5.12 lakh to roughly 2.6 lakh words

“When you give people simplicity, they embrace it,” said Nirmala Sitharaman, Union Finance Minister, at the launch of PRARAMBH 2026, a nationwide campaign to raise awareness about the Income Tax Act, 2025.

Crucially, the new law does not impose any new taxes. Tax slab rates are unchanged from FY 2025-26, and the zero-tax limit of ₹12 lakh under the new regime remains fully intact. This is a structural reform, not a rate hike.

Change 1: Goodbye “Assessment Year,” Hello “Tax Year”

This is the single most confusing thing for most taxpayers every year, and it’s finally been fixed.

Previously, income earned in one “financial year” (say, FY 2025-26) was assessed in a different “assessment year” (AY 2026-27). The two-year terminology tripped up salaried employees, small business owners, and even seasoned CAs.

Under the Income Tax Act, 2025, income earned between April 1, 2026, and March 31, 2027, is filed and assessed within the same period, called Tax Year 2026-27. This eliminates the confusion of earning in one year and assessing in another.

What this means for HR teams:

- Payroll software and internal compliance documentation will need to be updated to use the new terminology

- Employee communication materials such as offer letters, tax declarations, and salary slips should reflect “Tax Year” instead of “Financial Year/Assessment Year”

- Any queries from employees about their TDS should now reference Tax Year 2026-27

Change 2: New Tax Slabs? No. Existing Relief? Yes.

There are no new tax slabs for FY 2026-27. The most notable update is the higher basic exemption limit under the new regime, which allows tax-free income of up to ₹12 lakh, aimed at easing the burden on middle-income groups.

The old regime, with deductions under Sections 80C, 80D, and others, remains available, offering a choice based on individual financial behaviour.

Here’s a quick reference for the New Tax Regime slabs (which remain the default):

| Annual Income | Tax Rate |

| Up to ₹4 lakh | Nil |

| ₹4 lakh – ₹8 lakh | 5% |

| ₹8 lakh – ₹12 lakh | 10% |

| ₹12 lakh – ₹16 lakh | 15% |

| ₹16 lakh – ₹20 lakh | 20% |

| ₹20 lakh – ₹24 lakh | 25% |

| Above ₹24 lakh | 30% |

With the ₹75,000 standard deduction, salaried individuals earning up to ₹12.75 lakh effectively pay zero tax under the new regime.

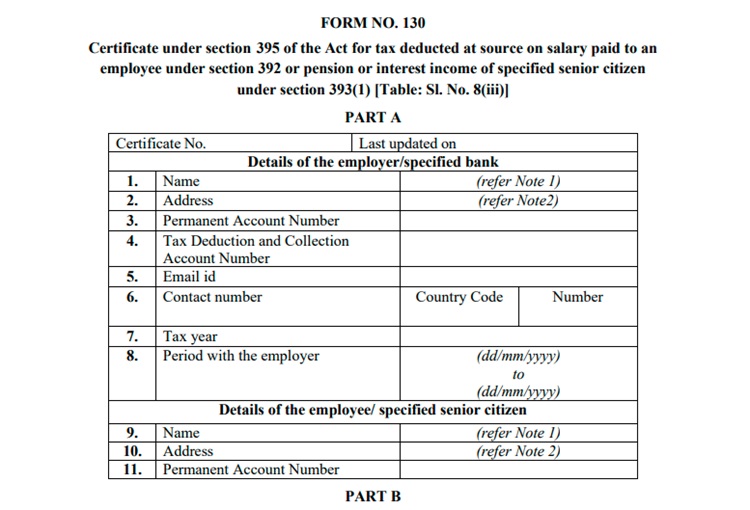

Change 3: Form 16 Is Gone; Meet Form 130

Every HR and payroll professional needs to act on this one immediately.

Form 16, traditionally issued by employers as proof of TDS on salary, has been replaced by Form 130 under the Income Tax Act, 2025. The name change sounds routine. The structural upgrade isn’t.

Unlike the two-part structure of Form 16, Form 130 uses a three-part structure: Part A covers deductor/deductee details; Part B shows TDS reconciliation; and Part C contains the detailed salary computation with exemptions, deductions, taxable income, and tax paid.

Form 130 also extends coverage to pensioners and certain senior citizens, a gap Form 16 didn’t address. Other commonly used forms have been renumbered, too:

| Old Form | New Form | Purpose |

| Form 16A | Form 131 | TDS certificate for non-salary income |

| Form 24Q | Form 138 | Quarterly TDS return filed by employers |

| Form 26AS | Form 168 | Annual tax statement |

Form 130 must be issued to employees by June 15 via the TRACES portal. It’s generated only after the employer files quarterly returns through Form 138; offline versions are invalid. Any delay or error in your quarterly TDS filing will directly hold up your employees’ ITR filing.

HR action points:

- Update payroll software to generate Form 130, not Form 16

- File quarterly TDS returns (Form 138) on time, or errors might cascade downstream

- Tell employees before June 15 that they’ll receive Form 130 this year, not Form 16

The form has a new name. The compliance responsibility is unchanged.

Change 4: Revised Return Deadline Extended to March 31

Under the Income Tax Act 2025, you now have longer to fix a filed return. Section 263 extends the revised return window from nine months to twelve months from the end of the tax year. This means that errors, missed deductions, or incorrect figures can be corrected up to March 31 of the following year, instead of the earlier December 31 cutoff.

A late fee applies if you file the revision after the nine-month mark:

| Total Income | Fee |

| Up to ₹5 lakh | ₹1,000 |

| Above ₹5 lakh | ₹5,000 |

Revisions filed within the first nine months remain free.

What this means for HR teams:

- Employees who receive corrected Form 130s, salary revision arrears, or late investment declarations now have more runway to file revisions

- Proactively communicate the March 31 window to employees, especially if your team issues TDS corrections or Form 138 amendments late in the cycle

- This extended deadline applies to Tax Year 2026-27 onwards (income from April 1, 2026). For AY 2026-27, the old Act applies, revised return deadline remains March 31, 2027

Change 5: More Cities Get 50% HRA Exemption

This is a significant win for employees in India’s growing metros and an important payroll update for HR.

Recognising demographic shifts and the growth of new economic centres, the 2026 Rules expand the definition of “Metro” cities for HRA calculations, allowing the enhanced 50% HRA exemption to a broader set of cities effective April 1, 2026.

The newly included cities are Hyderabad, Pune, Ahmedabad, and Bangalore, bringing the total to 8 cities under the 50% HRA exemption category, along with Delhi, Chennai, Mumbai, and Kolkata.

Why this matters for payroll:

- Employees based in these four cities can now claim 50% of their basic salary as HRA exemption, up from 40%

- HR teams need to update CTC structuring templates for employees in these locations

- This change makes a meaningful difference to in-hand salary for mid-to-senior level employees in Bengaluru, Pune, Hyderabad, and Ahmedabad

Change 6: Perquisites Get Updated for the First Time in Decades

This one’s long overdue. The allowances and perquisites under the old rules hadn’t kept pace with inflation or real-world costs for years.

The new rules now reflect exempt allowances and perquisite values that are consistent with current market rates and inflation, a change described as making exemptions and benefits meaningful, in contrast to the old rules.

Key updates include:

- Meal coupons: Meal vouchers up to ₹200 per day are now tax-free (up from the old ₹50 per meal limit)

- Children’s education allowance: Increased to match current school fee realities

- Hostel allowance: Revised upward

- Car perquisites: Motor car benefit valuation rules have been clarified and updated

For HR teams managing CTC structures, benefits administration, and flexi-benefit plans, this is the right moment to review what you’re offering and ensure the new limits are reflected in payroll software.

Change 7: Good News for Small Businesses and Freelancers

Small business owners with turnovers up to ₹10 crore will benefit from a strengthened presumptive taxation scheme, exempting them from maintaining detailed books and undergoing audit, if cash receipts are below 5%

“India’s small business owners and professionals are really the engine of our economy,” explained Finance Minister Sitharaman.

This matters for HR when hiring consultants, freelancers, or gig workers. If your vendor/contractor operates under presumptive taxation, the compliance requirements on their side have eased. This may reduce documentation delays in onboarding and payment processing.

Change 8: ITR Filing Deadlines, One Important Extension

The deadline to file ITR-3 and ITR-4 has been extended to August 31 from the end of the tax year. This also applies to FY 2025-26. However, the deadline for ITR-1 and ITR-2 remains the same, July 31.

Quick reference:

| ITR Form | Who Files It | New Deadline |

| ITR-1 (Sahaj) | Salaried individuals, one house property | July 31: unchanged |

| ITR-2 | Capital gains, multiple properties | July 31: unchanged |

| ITR-3 | Business/profession income | August 31: extended |

| ITR-4 (Sugam) | Presumptive taxation | August 31: extended |

| Tax audit cases | Businesses requiring an audit | October 31: unchanged |

Change 9: New Tax Rules for ESOPs, F&O, and Gold Bonds

Two changes specifically affect employees with Employee Stock Ownership Plans (ESOPs), stock holdings, or Futures and options (F&O) trading:

Buyback taxation: From April 2026, buyback proceeds will be taxed as capital gains instead of dividends. For retail investors holding shares more than 12 months, LTCG applies at 12.5% (above ₹1.25 lakh annual exemption). If held for 12 months or less, STCG applies at 20%.

Securities Transaction Tax (STT) on F&O: The STT on futures contracts increases from 0.02% to 0.05%, and on options contracts from 0.1% to 0.15% on the sell side. For employees who trade derivatives, this directly increases transaction costs. However, F&O traders who declare trading as a business can deduct STT as a business expense.

Dividend interest deduction removal: Under the old rules, investors could deduct interest expenses up to 20% of dividend income when computing their taxable dividend income. The amendment to Section 93 of the Income-tax Act 2025 disallows any interest deduction against dividend income or mutual fund income, effective April 1, 2026. This means investors who borrowed funds to buy dividend-yielding shares or mutual fund units will now be taxed on the full gross income, with no offset for financing costs.

Sovereign Gold Bond (SGB) exemption: Previously, anyone holding an SGB until maturity enjoyed a tax-free exit on capital gains, regardless of whether they bought it directly from the RBI or from the secondary market. Now, the exemption hinges on investor behaviour as only those who subscribed at the time of original issue and held the bond continuously until maturity will qualify for the capital gains exemption. Secondary-market SGB buyers, as well as those opting for premature redemption, will now be liable to pay capital gains tax: LTCG at 12.5% for holdings over 12 months, or STCG at the applicable slab rates for shorter holding periods.

Change 10: Uniform TCS Rate and Reduced MAT

Two more changes that affect businesses and finance teams:

- TCS simplification: Multiple TCS rates across categories have been consolidated into a uniform 2%, reducing confusion for businesses and importers and continuing the government’s effort to reduce TCS-driven refund delays.

- MAT reduction: Minimum Alternate Tax has been reduced from 15% to 14% for companies. Critically, companies will not be allowed to accumulate new MAT credit after March 31, 2026. Existing MAT credits accumulated before April 1, 2026, can still be utilised under current rules.

Change 11: Parallel Reading Utility: Government’s New Initiative

The Income Tax Department has introduced a new online comparison utility that allows taxpayers to check old and new provisions side by side. It’s called the Parallel Reading Utility, and it does exactly what HR and payroll teams need right now.

You pick a section from the old law using a dropdown menu, and the system automatically shows the corresponding section under the Income Tax Act, 2025. Users can also access the full text of both Acts directly from the same platform. No login required.

For example: Section 80C (deductions) → maps to its new clause under the 2025 Act. Section 192 (TDS on salary) → now consolidated under Section 393. Section 203 (Form 16) → now governed by Section 395, which prescribes Form 130.

If your team maintains any compliance checklists, employment contract templates, or HR policy documents that cite specific sections of the Income Tax Act, run them through this tool before the next payroll cycle. It’s a five-minute exercise that could save hours of confusion later.

What HR Teams Should Do Right Now

The new law doesn’t demand panic, but it does demand action. Here’s a practical checklist that can help you navigate these changes:

- Update payroll software to reflect revised allowance limits (meal coupons, education, hostel, car perquisites)

- Review HRA structuring for employees in Hyderabad, Pune, Bangalore, and Ahmedabad, as they now qualify for 50% exemption

- Revise CTC templates and offer letter formats to use “Tax Year” terminology

- Communicate to employees about the zero-tax threshold (₹12 lakh / ₹12.75 lakh for salaried) and the new ITR-3/ITR-4 deadlines

- Brief your tax consultants on the MAT credit deadline. Any unused credit strategy needs to be locked before March 31, 2026, has passed

In the End…

India’s tax overhaul isn’t about paying more or less. It’s about paying right, without needing a lawyer to decode a 5-lakh-word document. Revenue Secretary Arvind Shrivastava described the Income Tax Act, 2025, as representing not merely a new law, but a deliberate shift towards a simpler, clearer, and more user-friendly tax system.

For HR professionals, this shift comes at a time when payroll compliance is already under intense scrutiny, including the implementation of the Labour Code and DPDP Act obligations. Getting ahead of the April 2026 changes isn’t just good practice. It’s the difference between a smooth FY 2026-27 and a scramble when the first salary cycle kicks off under the new rules.

The law has been simplified. Now it’s your turn to simplify how your organisation responds to it.

FAQs

Here are the tightened FAQ answers:

What is the Income Tax Act 2025, and when does it come into effect?

The Income Tax Act 2025 replaces the 1961 Act effective April 1, 2026. It trims the law from 819 sections to 536 and cuts the word count from 5.12 lakh to roughly 2.6 lakh. No new taxes, no new slabs; it’s a structural simplification aimed at reducing compliance burden.

What is “Tax Year” under the new Income Tax Act 2025?

“Tax Year” replaces the old Financial Year / Assessment Year split. Income earned and assessed in the same period is now called Tax Year 2026-27, no more filing in one year for income earned in another. HR teams should update payroll documents, offer letters, and tax declarations to reflect this terminology.

What is Form 130 and how is it different from Form 16?

Form 130 is the new TDS certificate for salary, replacing Form 16. It has a three-part structure, deductor/deductee details, TDS reconciliation, and full salary computation, versus Form 16’s two parts. It also covers pensioners and certain senior citizens. Employers must issue it by June 15 via TRACES, after filing quarterly returns on Form 138.

Which cities now qualify for the 50% HRA exemption?

From April 1, 2026, Bengaluru, Hyderabad, Pune, and Ahmedabad join Delhi, Mumbai, Chennai, and Kolkata in the 50% HRA exemption bracket. Employees in these four newly added cities were previously capped at 40%. HR teams should update CTC templates accordingly.

What are the updated meal coupon and perquisite limits under the new tax rules?

Meal vouchers are now tax-free up to ₹200 per day, up from ₹50 per meal. Children’s education and hostel allowances have also been revised upward, and motor car perquisite rules have been clarified. HR teams should update payroll software and review flexi-benefit structures to reflect these new limits.

Has the ITR filing deadline changed for FY 2026-27?

ITR-3 and ITR-4 deadlines have been extended to August 31 (also applicable to FY 2025-26). ITR-1 and ITR-2 remain due July 31. Tax audit cases stay at October 31. HR teams should communicate the August 31 extension to any freelancers or consultants on the company’s vendor roster.

What should HR and payroll teams do immediately in response to the Income Tax Act 2025?

Five priorities: switch payroll software from Form 16 to Form 130; update HRA structuring for employees in Bengaluru, Pune, Hyderabad, and Ahmedabad; revise offer letters and CTC templates to say “Tax Year”; communicate the ₹12 lakh zero-tax threshold and new ITR deadlines to employees; and brief tax consultants on the March 31, 2026 MAT credit utilisation deadline.